7 min read

Whether you’re a new investor trying to discover what type of loan is best for an investment property, a long-term investor who is trying to stay current, or an entrepreneurial investor looking for new ideas, I welcome you. You are in the right place.

🎬 WATCH: 4 Best Types of Investment Property Loans

I remember my first piece of investment property. A buddy of mine and I were two young men looking to buy a house in a gentrifying neighborhood and flip it. We were two boneheads back then, thinking the process would be stupidly easy.

And if you would have asked me then what the right type of loan was for that investment property, I would have replied a bit like a smart-aleck:

“The one you go to the bank for, where you ask for money.”

Investment Property Loans Have Changed

Now, some of you reading this may be too young to know what I’m talking about, but I know there are some of you out there who, like me, remember the “stated income loan” days. Back then, a bank didn’t ask for a tax return. They didn’t ask for an income or financial statement.

🔎 Related: Financial Planning Process Guide for Investors and Families

I don’t think they even asked for a pay stub to confirm what I said I was making at the time. You would simply tell them how much you made, and they would loan you money accordingly. Yes, they were crazy times.

We ended up making every mistake under the sun, of course, as we all do in our younger days. We bought the house, we did all the work ourselves, and we flipped the house. My buddy then was transferred to a job a few states away. I got married … and my young wife and I ended up living in that house for 18 months. Was it a painful lesson? Yes, but a wonderful one.

Of course, we’re living in much different times now. If we flash forward to 2000, the economy melted down, as many of you may recall — and then seven or eight years later, the financial crisis took hold stateside and then around the world.

In this new economic norm — wherein you’ll certainly need more than a firm handshake to “prove” your income — there are four types of loans you may want to consider for an investment property. In this article, we’re going to go through each of them at a general level, so you can point yourself in the right direction of what may make the most sense for you. (Although, we’re here as a resource if you have questions about your specific set of circumstances.)

Loan #1: Conventional Bank Loan

This is your standard process of walking into the bank, sitting down with a lender, and providing them with three to five years of tax statements demonstrating your cashflow in and out. There’s a good chance some of you have been through something similar to this process before, but here is where this type of loan differs from what you may be used to.

You’re typically going to put down 20% on your terms. Your amortization schedule is probably going to be shorter and your interest rate is going to be higher.

🔎 Related: What’s the Difference Between Real Assets + Financial Assets?

If this is an investment property for you, then you need to have a plan for how you are going to make a profit from this investment. Moreover, the bank will probably want to see that plan. For instance, if you plan to rent out this property, the bank will want to see how much you plan to rent it out for, as well as how you’re going to attract renters to the property.

Other questions you can anticipate include:

- Do you plan to hire a property management company?

- What do you believe you'll gain in rent on a monthly basis?

- How do you prove that? What is the data supporting this?

What this illustrates is the precise reason why I like conventional bank loans. If you’re working with a good banker — and by “good banker,” they are looking to sell you money, but they also have their own job on the line — they can give you great advice in these areas. If you’re working with a younger lender (or you may be a young lender), please don’t take offense to this, but I encourage you to become that good banking advisor to them, not just someone who sells money.

Loan #2: Bridge Loan

Some people refer to a bridge loan as a “hard money loan,” but no matter what you call it, the principle remains the same. Typically, you use this loan in the short-term, if you intend to flip a property or you’re having trouble securing a loan, and need a quick and easy fix.

🔎 Related: What Are the 4 Types of Investments Every Investor Must Know?

Now, banks generally won’t even consider something like this for you if you don’t already have a great pre-existing relationship with them. And again, yes, it is a quick and easy fix, but it’s not without its distinct disadvantages.

The interest rates are typically higher. The terms are short-term, and a balloon payment is owed within a short period of time. It may also be measured in months — six, nine, 12, 18, 24, 36, and so on — and you will owe the entire principle at the end of that period of time.

Let me give you a word of warning about bridge loans. If reputable lending institutions are not willing to loan you money on an investment property, you need to take a step back, be very self-aware, and ask yourself:

“Why might this be a bad idea that I need to stay away from?”

Ask the banks themselves, too. Yes, sometimes you may really just need money in a quick bridge sort of way, and this can be the solution that works best for you. Just engage with this option thoughtfully and with intention.

Loan #3: Private Money

This loan is one that is exchanged between two private individuals. Now, because these loans are private transactions, there isn’t a lot of public data about their efficacy. But this type of loan has been around for generations, and they’ve become increasingly popular in recent years as wealthier investors are looking for private investment opportunities.

🔎 Related: How Does Sound Financial Make Client Investing Decisions?

Loan terms and rates will, understandably, vary widely across the board. Typically, if this is an “arm’s length” transaction in a private money sort of way, then you will not get a “friend” deal. Meaning, your terms are probably a little more strict, but they can be more flexible.

For example, you may pay a higher interest rate to get more flexibility on the amortization. Or you could pay a lower interest rate, but to lock it in over a long period of time there may be some steep prepayment penalties. You simply need to know as the investor, as the borrower, what you’re getting yourself into and, to the best of your ability, shape that loan to fit the type of investment you’re trying to make.

Loan #4: Home Equity Line of Credit (HELOC)

If you’re a homeowner, you can use the equity in your home as collateral at your bank to borrow money to purchase another property. This is very common, and if you know what you’re doing, it can be effective.

Even if you’re familiar with it, your bank should walk you through the process, it makes the paperwork a heck of a lot easier. Plus, they already have a relationship with you. They already have your information on file, you’re not going to need three years of tax returns, and so on. Sure, you may need to deliver your most recent tax statement, but you won’t need to go through the same deep excavation of your finances as you’ve done before.

🔎 Related: How Much Does Investment Management Cost?

If you’re an investor using a HELOC as a personal bridge loan, I like this idea a lot. It’s quick. It’s easy. You’re working with a known institution. However, as interest rates are higher today, as I’m recording this in early 2024, they are not the value they once were. So, if you’re facing a 7% to 10% interest rate on that line of credit, it’s not a good long-term lending mechanism for you.

Don’t Try to Fit a Square Peg in a Round Hole

When you’re looking at any of these types of loans, I strongly recommend you look at their design and understand the intent of the loan. If it is designed for a long-term lending process, then use it as one. If it's designed for short-term use, then use it as one. Don't try to fit a square peg in a round hole by using a loan in a form that it was not meant to be used.

🔎 Related: What Are the 4 Risks of Investing? (+ Examples)

How do you know how it's meant to be used? Go study the loan. Look at the terms, think about the process, think that process through, and see if it fits your investment property. Typically, I preach for you to be relatively debt-free. I use the word relatively because there's reasons to use debt wisely. But a mature investor, a wise investor, thinks they're smart, they study the process and they use it to their advantage.

Are there pros and cons to each of the types of loans I discussed here? Absolutely, and we reviewed a few of those together. But again, this is where you need to take ownership and become a student of these loans and think through what these processes will mean for you.

Yes, using the bank’s money instead of your own is a good idea. However, profit from real estate investments are subject to the ups and downs of the U.S. economy. So, beware and do not build a house of cards. I've seen this far too many times in the investment space where someone keeps levering up their assets to buy more assets and effectively they've got a lot of paper ownership of properties.

There Are Times to Take Risks in Investing

I know this, I've done this. I'm with you on that. There are times to put the pedal on the floor. But there are also times to wisely pay off debt, consolidate your assets, and grow your business securely over time. And that's what I want you thinking about as you're considering using debt to grow your property portfolio.

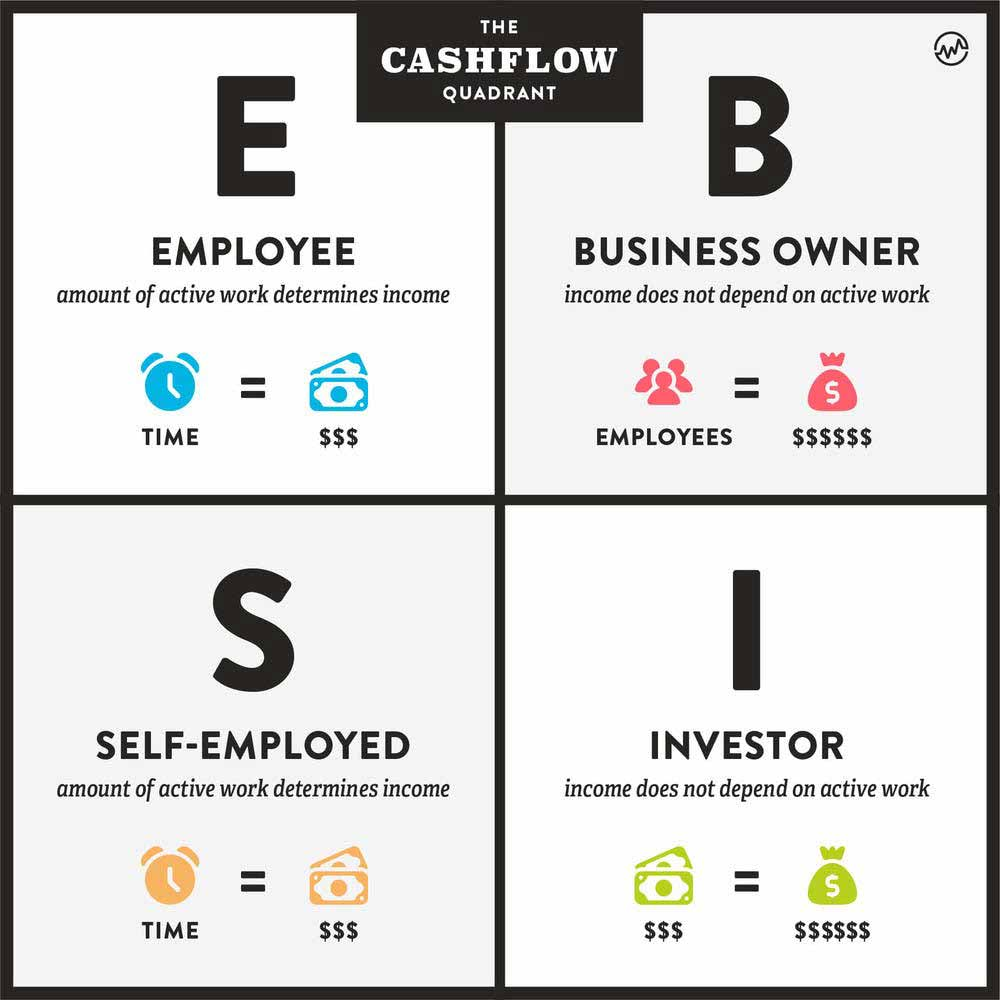

Source: Robert T. Kiyosaki

Robert Kiyosaki’s Cashflow Quadrant is a great reference for what I encourage you to think about as you look ahead to your investments.

In this diagram, Robert talks about how people earn money as an employee (E) or self-employed as a business owner (B), a business owner (B), or an investor (I). If you're borrowing money to purchase investment properties, you are attempting to be an I (an investor), but you must think like a B (a business owner) and develop your asset management system, manage your cashflow and pay off your debts.