6 min read

Investing after retirement is an exciting topic, but it is one you must enter into with great care and purpose. More specifically, you need to bring more focus to what you want to accomplish through your investments than you may have when you thought about investing prior to retirement.

Back then, “grow my money” may have seemed like a sound investing goal. And if that’s how you approached it, I don’t blame you. That’s how we’re trained to think about our money. Money is both the means and the end, right?

🔎 Related: How much does investment management cost?

Well, not quite. One of our founding principles at Sound Financial is that when you start thinking of money as a tool, rather than the ultimate goal, you can greatly expand what is possible. And this is even more true when we’re having post-retirement investment conversations.

To focus broadly on “growing your money” through retirement investing is essentially investing in luck, while also increasing your risks of failure.

So, when we think about investing after retirement, ask yourself:

- Are you trying to leave an inheritance?

- Are you simply looking to increase your income?

- Do you have new post-retirement goals you’re looking to make possible?

The more specific you can be with your goals, the better. With that in mind, let’s talk about what you need to know about investing after retirement … because a lot has changed.

The retirement landscape has changed

So many of the investing decisions you’ll make post-retirement will depend on timing (what’s happening in the market), where an “investing in luck” with nebulous goals simply will not work. Even if you have a higher risk tolerance than some, retirement is not the time to gamble.

🔎 Related: Investment strategy, the Sound Financial way

For example, if you retired in late 2023, you retired into one of the highest stock market valuations on record — a very different set of circumstances than if you had retired following historic stock market carnage in 2009.

On top of that, we’ve become a healthier population with greater life expectancies:

- 1930: 58 years (men), 62 years (women)

- Present day: 73.5 years (men), 79.3 years (women)

While our ability to live longer, happier, and healthier lives is something that should be celebrated, we must also recognize that many of the retirement and post-retirement support mechanisms we’ve established as a society were designed with older life expectancies in mind (and have not been updated).

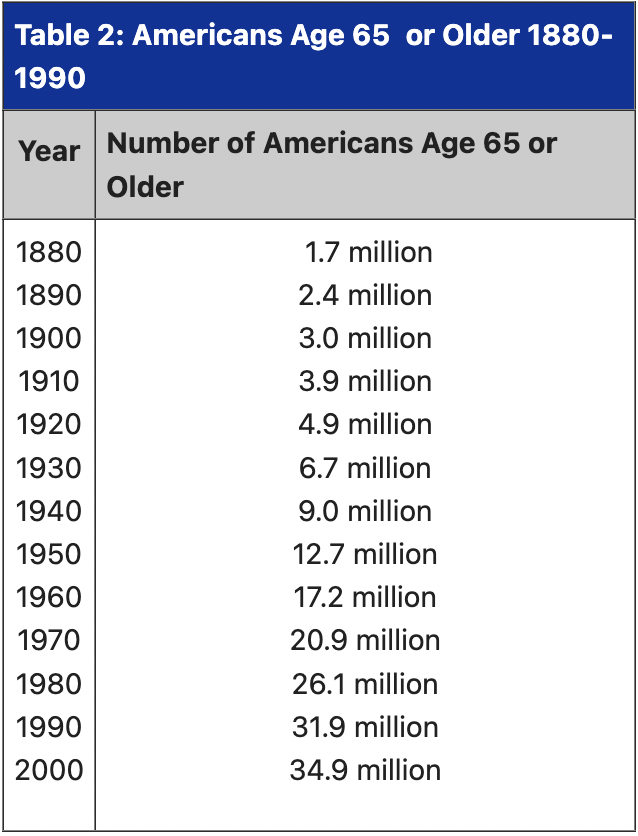

For instance, Social Security was established in 1937. Today, folks are living much, much longer:

As a result, many of these programs some of us may have thought of as guarantees are under greater strain than ever before.

Then we need to consider the volatility of the economy over the past few decades, and how that has influenced how we view retirement, as well as our ability to plan for it effectively. Let's be fair to ourselves. The economy has always been volatile, we just now have 24-hour news channels to constantly tell us how "bad" it is.

🔎 Related: Asset vs. wealth management (What’s the difference?)

However, it is true that in many ways, we were not able to build a proper retirement portfolio for the past 15 years because interest rates were so low. Now, interest rates are back to historical norms, we are better able to build income producing portfolios with the stability needed to reach your retirement goals — at least for a while.

When we evaluate these influencing factors collectively, we see we must look elsewhere for the financial security we seek in our retirement years, with a clear vision of our goals. For some of you, this may mean through investments. So, let’s talk about that.

Your post-retirement investment goals

We’ve already discussed the importance of having concrete goals for your post-retirement investment strategy, but let’s take a look at an example to show you why it’s important. Let’s imagine for a moment we’re working together, and you’ve got a big, exciting post-retirement goal you want to make a reality.

Maybe you want to hop in an RV with your spouse, your best friend, or a significant other to travel all over North America, to see this nation’s glory — from the Grand Canyon to Niagara Falls, and everywhere in between. You plan to do most of your traveling during the warmer months, and then you’ll return home during the winter to celebrate the holidays and rest.

🔎 Related: How does the U.S. economy work? (an accessible overview)

Or perhaps you have quite a different vision for yourself. You’ve always wanted to work with a particular ministry as a volunteer, and now is your chance. Of course, you still need income to live off of, while you live out your passion of helping others.

Heck, maybe your lifelong retirement dream is simply to stay at home and spoil your grandkids rotten, whenever you have the chance.

No matter what, at some point you’ll turn to me and say:

“Chris, help us make that happen.”

Transforming retirement plans into reality

This is where we translate your vision for the future — an emotional idea — and transform it into something logical. You have to be very honest with yourself at this step. For example, you should not take more than 4% of your investments out for your income, unless your fixed rate guarantees you more than 4%.

This may work well for you, or you may have to engage in part-time work to supplement your income. When you have a clear idea of what you want your retirement life to look like, it will be much easier for us to understand precisely what actions you need to take to guarantee you have the income you need in these golden years.

🔎 Related: How to choose a financial advisor (tips + questions to ask)

It’s also at this point that you’ll want to avoid idealizing what you believe your spending habits will be.

For instance, it’s not uncommon for folks to think they’ll do most of their retirement spending in the first five to 10 years, and then reduce their spending significantly as they get older. Sure, you may be traveling less as you get older, but your medical bills may increase, or you may have new expenses to consider, such as a nursing home.

Again, this is why investing after retirement may be something you want to consider. It is possible to grow your wealth (with clear goals) after your prime income years. And it may be wise to do so, depending on if your goals changed or how changing times (and markets) may have impacted your post-retirement income picture.

The classic 60/40 portfolio

This is not a post-retirement investment recommendation, but the classic 60% stocks, 40% bonds portfolio model is a classic for a reason. It is not only highly tested in theory, but it has also been used for decades in fact.

🔎 Related: What are investable assets? (definition + examples)

That said, the security selection of what goes into that 60/40 matters tremendously, and it changes over time, depending on the market environment we’re in. This is where you need to make a point to become educated — on your own and/or working with a financial professional.

Yes, this can be learned, and it’s imperative that you do so before you make investment choices of any kind.

You cannot take traditional portfolio models at face value, nor should you take advice from friends or family members who (in all likelihood) are living out different financial circumstances than you are. Even that best friend of 40 years you’ve got, so close you’ve shared a tackle box.

Their journey is their journey, and your journey is your journey. You cannot draw parallels.

Don’t bet on luck in retirement, invest smart

Yes, you may run into folks who have gotten lucky with their investments in the past 15 years. But as I’ve said throughout this, you cannot bet on luck. Because even if you have lucky moments of your own, luck is not something you can plan for — it also almost always runs out.

🔎 Related: 7 best compound interest investments (overview + examples)

When you’re younger, losses will still hurt, but time is on your side. You have more years to refine your investment strategies and build toward your retirement goals. Once you’ve crossed into retirement, those luck-based losses can be much more painful.

When luck runs out during retirement, you may find yourself in a scenario in which you must come out of retirement. You have to go back to work. That is the risk you run when you’re chasing growth as a goal, instead of dialing in what you really want out of these years and making a clear plan of action to attain it.

Of course, don’t let fear of loss rule you too greatly either. While there is certainly such a thing as a portfolio that isn’t conservative enough, you can also swing to the other extreme where your portfolio is too conservative, where opportunities are missed.

For example, we’ve talked before about why sometimes the stock market has a reputation for being similar to gambling. To carry that analogy forward here, another thing to keep in mind is that yes, in our stock market, sometimes “the house wins.” In 2022, the house won and took a lot of people’s money. In 2023, it started to give some back. When that happens, you need to take advantage.

Retirement is exciting, but also emotional

Be kind to yourself in this regard, because you are moving into an entirely different phase in your life. Similar to other firsts in our lives — going to college, getting your first job, getting married, buying your first house, etc. — retirement is a first that we are often not fully prepared for, in terms of what these changes actually look like in practice.

Before and after retirement, you will have to make a lot of decisions and, as changing times, economic environments, and the stock market have shown us, there are very few guarantees. For some of you, this may mean that you’re in a retirement reality that isn’t quite what you imagined.

The key thing to keep in mind right now, particularly when talking about investing after retirement, is that while this can be an emotional time, you should not make emotional decisions, no matter what those emotions may be. Live life as it is, do not judge your success or failure in retirement as success or failure in life. Again, be kind to yourself.

And, when in doubt, reach out to a financial advisory professional. We’re always here to answer your questions and help you achieve your goals.